⏱️ Read Time: 3 Mins

The FAFSA processes, the confirmation email arrives, and the math immediately looks completely wrong. A graduate student staring down a $75,000 annual tuition bill checks their estimated federal aid, only to find a loan limit capped right around $20,500. The missing money isn’t just a rounding error. It feels like the Grad PLUS loan just disappeared.

But that missing number is not a glitch, and it is certainly not a denial. The system is operating exactly as it was built.

If your FAFSA shows a number but it’s too low, that’s a different problem.

The part the system doesn’t show

This is where people get confused. The Free Application for Federal Student Aid is an intake form, not a final lending contract. When a graduate or professional student pushes submit, the federal system only calculates base-level entitlements.

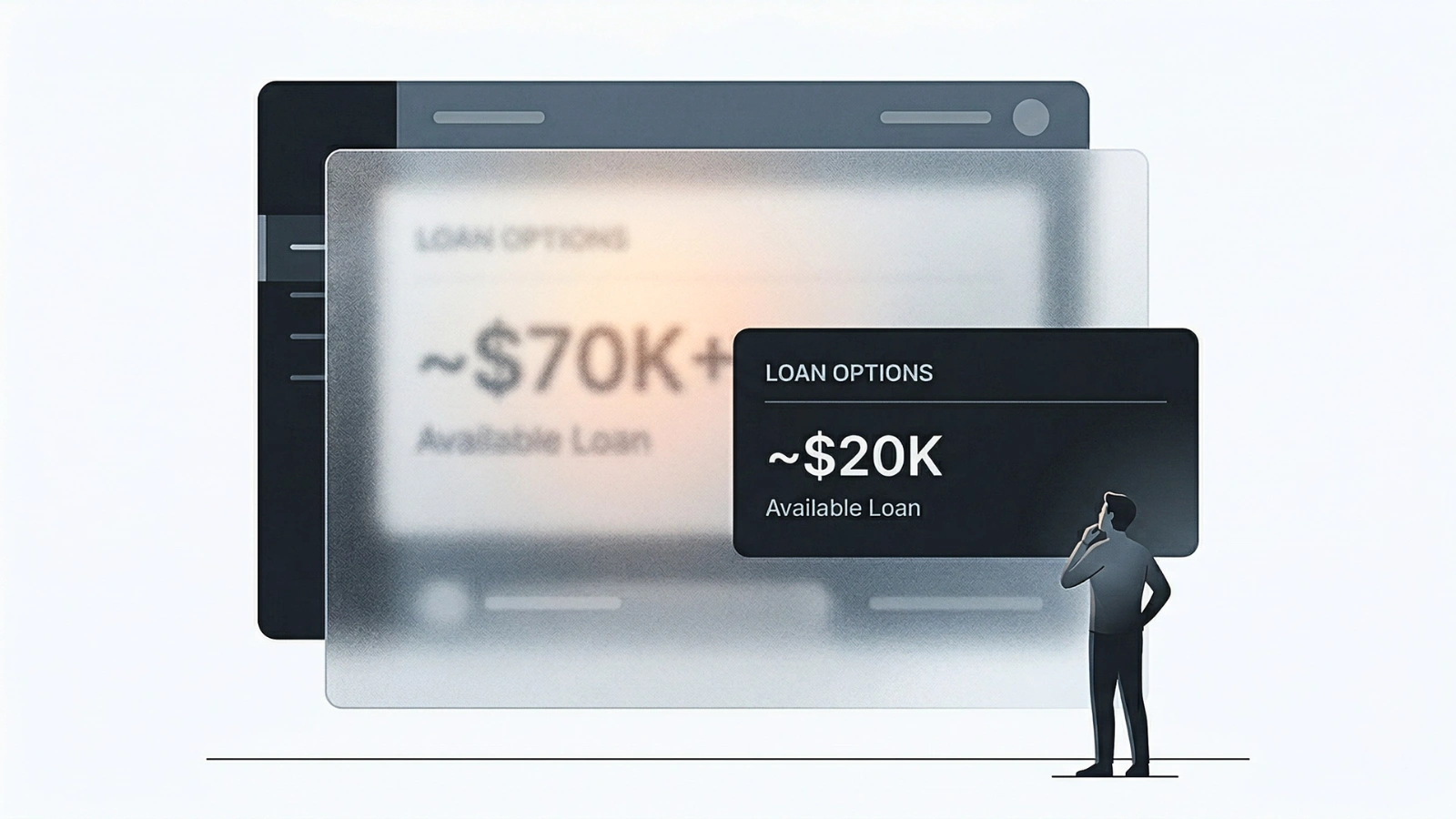

By federal law, graduate students are entitled to a maximum of $20,500 per academic year through the Direct Unsubsidized loan program. Because this loan is a statutory guarantee requiring no credit check or co-signer, the FAFSA algorithm can calculate it instantly and display it on the confirmation screen.

The algorithm stops right there. It does not project or promise anything beyond that base entitlement. Even if tuition is four times higher, the federal summary screen will not move past the $20,500 ceiling.

That’s the part no one tells you.

FAFSA Submitted But No Aid Offer Yet? What Happens Next

Financial Aid Disbursed But No Refund? Here’s Why

Where the missing money actually comes from

The Grad PLUS loan is the financial bridge between the $20,500 base loan and the actual cost of attendance. Students can borrow up to the full published cost of the program minus other aid.

It doesn’t show up on the FAFSA estimate because the Department of Education cannot pre-approve a credit-based product on a demographic application. Unlike the base loan, the Grad PLUS program requires a credit check to screen for bankruptcies, liens, or severe defaults.

Since FAFSA does not pull credit reports, the system has no authority to display PLUS loan estimates. It leaves the field blank rather than making a promise it cannot legally back up.

This screen is not your actual offer

The confirmation email from Federal Student Aid is just a data receipt. It confirms submission and calculates the baseline guarantee. It is not the actual financial aid package.

The real packaging happens at the university. The financial aid office downloads FAFSA data, applies institutional costs, and builds the award letter. That is when the Grad PLUS loan appears alongside the unsubsidized loan and any scholarships.

How to Increase Your Loan Limit with a Cost of Attendance Appeal

FAFSA Loan Amount Too Low? Here’s What It Really Means

What you should actually do now

Calling the federal help desk about the missing PLUS loan is pointless. Representatives cannot add it to the screen or bypass the credit requirement.

The process shifts to the school’s timeline. Once the university issues the award letter, they provide instructions for unlocking PLUS funds. This requires logging back into the federal portal, completing a separate Grad PLUS application, and consenting to the credit check.

The money is there for any borrower without severe credit issues. FAFSA did its job by loading baseline data. The rest of the funding waits for the university to trigger the next step.

Loan rules are changing starting mid-2026, and new borrowers may not see Grad PLUS as an option, but this structure still applies to current aid estimates.

Sarah Johnson is an education policy researcher and student-aid specialist who writes clear, practical guides on financial assistance programs, grants, and career opportunities. She focuses on simplifying complex information for parents, students, and families.