⏱️ Read Time: 3 Mins

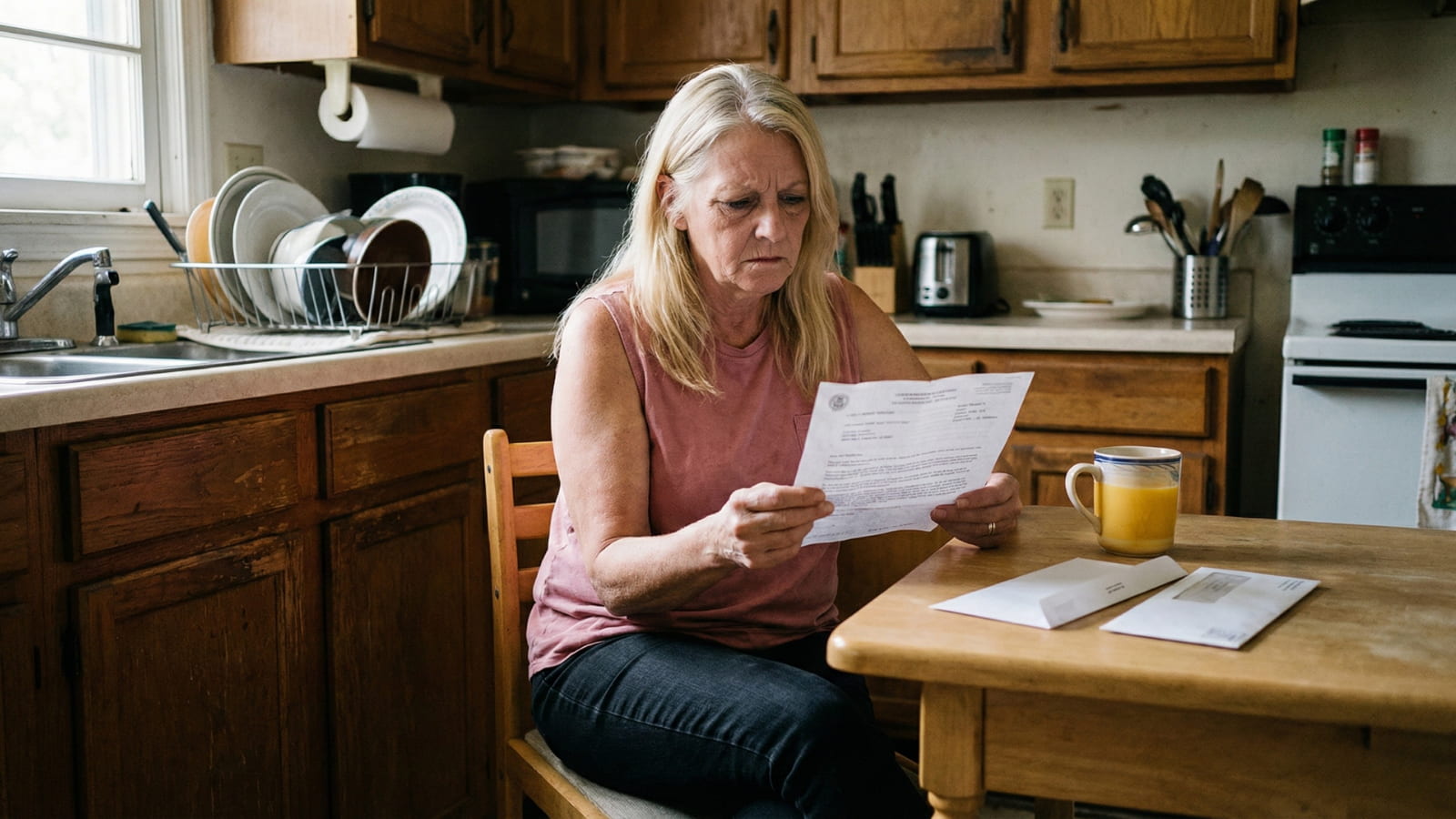

Robert checked his mailbox on the third of the month, completely unaware that a Social Security Seizure was waiting inside.

He ripped open the envelope from the Social Security Administration, expecting his usual deposit of $1,800.

It was $1,530.

There was no explanation in the envelope, just a lighter check. He called the bank. They blamed the government. He called the Social Security office. They told him to call the Department of Education.

Robert had just discovered the “offset.”

He assumed his student loans from the 1990s, which he had stopped paying a decade ago when his carpentry business went under, were ancient history. He thought they had “fallen off” his record like a bad credit card debt.

He was wrong. And in 2026, millions of seniors are waking up to the same reality: The federal government does not have a statute of limitations.

Private Creditors vs. the Federal Government

To understand why this happens, you have to understand the difference between a bank and the U.S. Treasury.

If you default on a Visa card or a private car loan, the lender can sue you. But they cannot touch your Social Security. Federal law (Section 207 of the Social Security Act) creates a “legal fence” around your retirement benefits. Private debt collectors cannot cross it.

The Department of Education operates under different rules.

Under the Treasury Offset Program (TOP), federal student loans are exempt from that protection. If you are in default, the government can legally bypass the courts and garnish up to 15% of your monthly Social Security check automatically.

They don’t need to sue you. They don’t need a judge’s signature. They just take it.

For a full explanation of the laws behind this seizure, read our guide on Why Social Security is Vulnerable.

The $750 Safety Net (and Why It Fails)

There is one specific rule that stops them from taking everything. It is known as the Financial Floor.

The government is legally forbidden from garnishing your check if it would leave you with less than $750 per month.

Here is how the math works for two different retirees:

- Retiree A (Gets $2,000/mo): The government takes 15% ($300). The retiree keeps $1,700.

- Retiree B (Gets $800/mo): The government cannot take the full 15% ($120) because that would leave them with $680. Instead, they take only $50, leaving the retiree with exactly $750.

The problem? This $750 floor was set in 1996 and has never been adjusted for inflation. Here is the insult to injury: The new ‘One Big Beautiful Bill Act‘ of 2026 overhauled student loans and repayment plans, but it completely ignored this rule. It left the offset floor at $750, the same level it has been since 1996. While the cost of bread has tripled, your protection level hasn’t moved a penny.

In 2026, $750 does not cover rent in almost any city in America. It barely covers food and utilities. Yet, the computer system treats anything above that amount as “disposable income” ready for seizure.

How to fight back (the hardship claim)

If your check has been hit, you do not have to accept the cut.

The computer system processes these garnishments automatically, but it has an override switch. You can file a Financial Hardship Claim.

To do this, you must contact the Treasury Offset Program or the Default Resolution Group at the Department of Education. You will need to fill out a Statement of Financial Status.

You must prove that the 15% garnishment prevents you from paying for:

- Food

- Housing

- Medical care

If you can prove that every dollar of your Social Security is needed for basic survival (which is true for almost everyone relying on it), they can suspend the garnishment entirely.

📄 Download the Hardship Form

Do not wait for them to mail it to you. Download the official “Statement of Financial Status” package here to start your claim immediately.

The Critical First Step

If you receive a “Notice of Intent to Offset” in the mail, do not throw it in the junk pile. The clock starts ticking the exact day the ‘Notice of Intent to Offset’ is printed. You have a strict 65-day window to file your objection. If you file on Day 66, they can legally ignore your request and seize your check anyway. Do not wait for the mail to be slow.

You have a 65-day window from the date on that letter to request a review or file a hardship claim before the money is taken.

Once the first check is garnished, getting that money back is nearly impossible. The goal is to stop the hand before it reaches into your pocket.

📞 Who to Call (The Direct Lines)

Do not call the main Department of Education number. You will be stuck on hold. Use these direct specific numbers to save hours of frustration.

-

To Check the List: Call the Treasury Offset Program (TOP) automated line at 800-304-3107.

-

To Stop the Seizure: Call the Default Resolution Group immediately at 800-621-3115.

Financial Health

Are You “Legally Insolvent”?

If you are facing a Social Security offset, your debts likely exceed your assets. This “Insolvency” status can actually protect you from tax penalties if your loans are eventually forgiven.

Sarah Johnson is an education policy researcher and student-aid specialist who writes clear, practical guides on financial assistance programs, grants, and career opportunities. She focuses on simplifying complex information for parents, students, and families.