⏱️ Read Time: 4 Mins

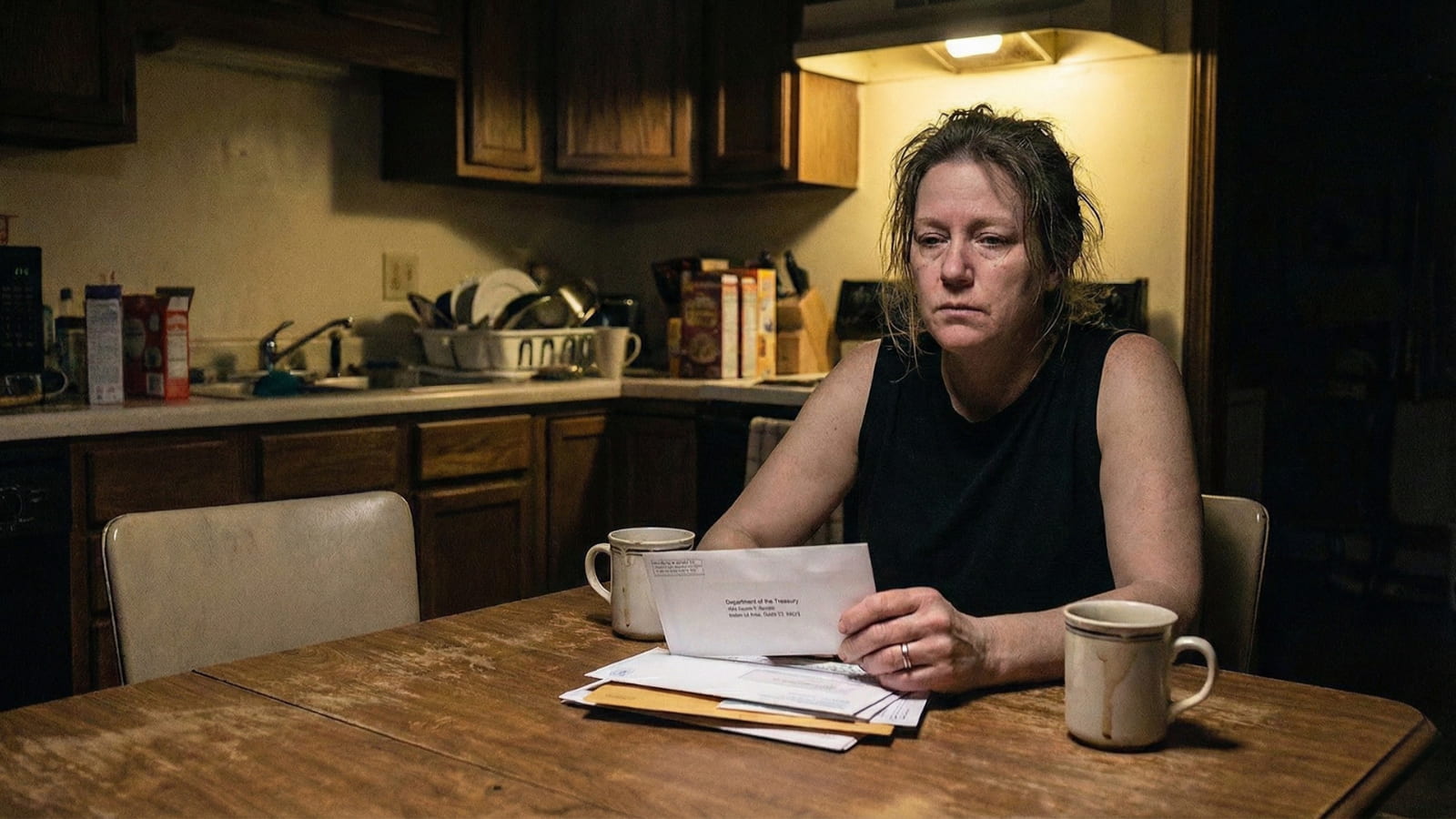

James makes $85,000 a year. He has a 780 credit score. He has $20,000 in savings.

On paper, he is the perfect homebuyer.

But when he walked into a major national bank last week to get pre-approved for a starter home, the loan officer looked at the computer screen, frowned, and handed him a rejection letter.

The reason? “Excessive Debt-to-Income Ratio.”

James was confused. He drives a paid-off Honda. He pays his credit cards in full every month. His only debt is $100,000 in federal student loans, which are currently on an Income-Driven Repayment (IDR) plan. Because his income is moderate, his required monthly student loan payment is exactly $0.

The bank didn’t care.

James just became the latest victim of the “1% Trap,” a lazy underwriting shortcut that big banks use to deny mortgages to perfectly qualified buyers.

If you have high student debt and low monthly payments, this math error is likely standing between you and your house keys.

How Banks Invent Monthly Payments

To understand why James got denied, we have to look at the invisible numbers the bank added to his application.

Mortgage lenders live and die by the Debt-to-Income Ratio (DTI). They add up all monthly debts and divide them by gross income. If the number exceeds 45% (sometimes 50%), the loan dies.

The problem arises when a student loan payment shows up as $0 on a credit report.

Conventional underwriting guidelines often panic at zeros. Instead of doing the work to verify the IDR plan, many large banks default to a brutal internal policy: The 1% Rule.

They take 1% of the total loan balance and “impute” it as a monthly payment.

For James, the math destroyed his future:

- Total Student Debt: $100,000

- Actual Payment: $0

- Bank’s “Fake” Payment: $1,000/month (1% of $100k)

The bank’s software artificially added a $1,000 monthly obligation, roughly the cost of financing a Tesla Model S, to his file. That single, non-existent expense pushed his DTI over the limit and triggered the rejection.

The 0.5% Calculation Rule

There is a way to delete half of that fake debt instantly.

It doesn’t involve paying off the loans. It involves changing the loan program.

While conventional loans (Fannie Mae/Freddie Mac) can be strict about student debt, the Federal Housing Administration (FHA) has a government-mandated rule that is much friendlier to borrowers in this specific trap.

It is hidden deep in HUD Handbook 4000.1, and it is called the 0.5% Calculation.

The Rule: If a borrower’s student loan payment is reported as $0, FHA lenders are instructed to use 0.5% of the outstanding balance for DTI calculations.

(Crucial Note: If the credit report shows an actual payment amount greater than $0, they use the actual amount. But for those stuck in the $0 deferment/IDR trap, the 0.5% rule is the default).

The Math That Saves the Deal

Let’s re-run James’s application through an FHA lender instead of a conventional bank.

- Conventional Bank Calculation: $1,000/month liability. (Denied)

- FHA Cheat Code Calculation: $500/month liability. (Approved)

By simply switching the paperwork, the lender slashed the “phantom debt” by 50%.

In the world of mortgages, freeing up $500 of monthly cash flow is massive. At current interest rates, an extra $500 a month roughly equates to $60,000 to $70,000 in purchasing power.

That is the difference between being priced out of the market entirely and signing the closing papers on a 3-bedroom colonial.

Why Your Bank Didn’t Tell You

It seems criminal that a loan officer wouldn’t mention this.

The reality is less malicious and more bureaucratic. Many big-box banks have “overlays”, extra rules they add on top of federal guidelines to minimize risk. A bank might know about the FHA rule but refuse to use it because their internal policy is strictly “1% across the board.”

They aren’t technically lying when they say “we can’t approve you.” They mean “we” (this specific bank) cannot approve you.

Why You Should Avoid Big Banks

If you are holding six figures of student debt, do not apply for a mortgage through a banking app.

You need a human Mortgage Broker.

Brokers are different from bank loan officers. A bank officer works for the bank and sells only that bank’s products. A broker works for you and shops your file across dozens of wholesale lenders.

When interviewing a broker, ask one screening question:

“I have student loans on an IDR plan showing $0 payments. Do you have lenders who follow the FHA 0.5% guideline without overlays?”

If they hesitate, hang up. If they say “Absolutely,” you have found the person who can unlock the front door.

Financial Health

Is Your Debt “Solvent”?

If you have high student debt (like James), your Liabilities might exceed your Assets. This “Insolvency” status can actually protect you from future tax bills.

🔒 Private & Secure. No login needed.

Sarah Johnson is an education policy researcher and student-aid specialist who writes clear, practical guides on financial assistance programs, grants, and career opportunities. She focuses on simplifying complex information for parents, students, and families.