Published: December 17, 2025

You log in to check your loan. Instead of a simple “Bill Due,” you see a status code: “Awaiting Form Administrative Forbearance” or “In-School Deferment.”

The difference between these words is not just semantic. Each status triggers a different set of rules for interest accrual, repayment schedules, and forgiveness eligibility.

MOHELA displays these statuses to reflect the current backend condition of the loan file. They indicate whether the billing engine is active, paused, or pending data.

This analysis reflects reported MOHELA servicing practices and federal loan regulations as publicly available through late 2025 and early 2026 guidance.

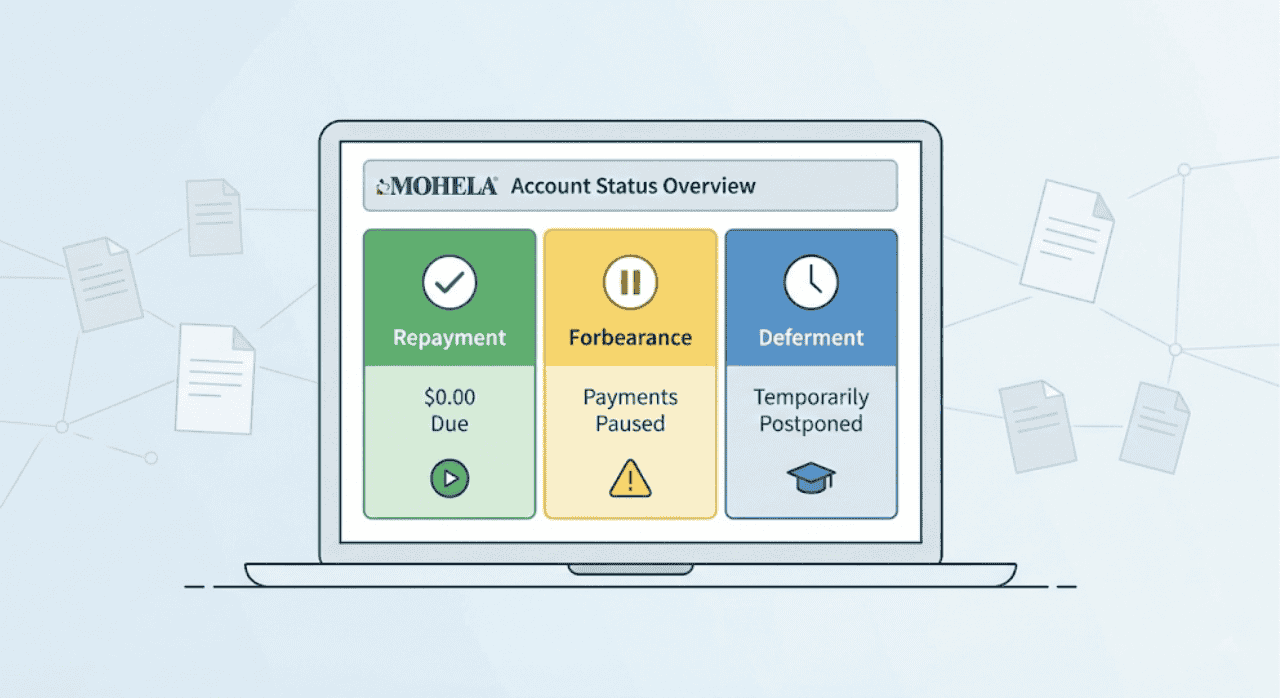

Repayment: The Active State

“Repayment” is the standard operational status. It means the loan is active, a bill is being generated, and a payment is required.

When a loan is in Repayment, the specific amount due depends on the selected Repayment Plan (e.g., SAVE, IBR, or Standard).

It is possible to be in “Repayment” with a $0.00 amount due. This occurs for borrowers on Income-Driven Repayment (IDR) plans whose income is below the poverty guideline threshold.

Even if the payment is $0, the status remains “Repayment” because the account is satisfying the monthly obligation.

This status can count toward Public Service Loan Forgiveness (PSLF) and IDR forgiveness when all program requirements are met.

Forbearance: The Temporary Pause

“Forbearance” indicates a suspension of payment requirements. During this period, the borrower is not required to make payments, and delinquency does not occur.

The critical factor in Forbearance is interest.

In most general forbearance scenarios, interest continues to accrue on many loan types, including unsubsidized federal loans.

MOHELA dashboards often display specific subtypes of forbearance:

- Administrative Forbearance: Applied by the servicer during transfers, platform updates, or litigation holds (like the SAVE plan block).

- Awaiting Form Administrative Forbearance: Applied automatically while MOHELA processes a submitted document, such as an IDR application or consolidation request.

- General Forbearance: Typically a discretionary pause requested by the borrower due to financial difficulty.

While administrative forbearances protect credit reporting, they do not always count toward formal forgiveness progress.

Current Department of Education guidance suggests that certain administrative pauses, such as those for platform transfers, may count toward PSLF, while others, like the SAVE litigation pause, generally do not.

Deferment: The Entitlement Pause

“Deferment” is a pause granted because the borrower meets specific legal criteria, such as being enrolled in school, unemployed, or undergoing cancer treatment.

Deferment differs from Forbearance primarily in interest subsidies.

For Subsidized Direct Loans, the federal government typically pays the interest during a Deferment period.

For Unsubsidized loans, interest generally accrues, similar to Forbearance.

MOHELA applies Deferment statuses based on external data (like enrollment files from schools) or borrower applications (like Unemployment Deferment forms).

Because Deferment is an entitlement defined by law, it often has rigid start and end dates compared to the more flexible timelines of Forbearance.

“Awaiting Form” Status Indicators

A common and confusing status on the new MOHELA platform is “Awaiting Form Administrative Forbearance.”

This status appears when a borrower submits paperwork, such as an income recertification or plan change, that triggers a processing queue.

The system places the account in this holding pattern to prevent a bill from generating while the new payment amount is calculated.

Interest may continue to accrue during this processing window, depending on loan type.

Borrowers often see this status persist for 30 to 90 days depending on backlog volumes at the servicer level.

Grace Period

“Grace Period” is a specific status for loans that have recently left “In-School” status but have not yet entered “Repayment.”

This typically lasts for six months after graduation or dropping below half-time enrollment.

During the Grace Period, payments are not required.

However, for most loans disbursed after mid-2012, interest accrues during the grace period.

Once the six-month clock expires, the status automatically converts to “Repayment,” and the first bill is generated roughly 30 to 45 days later.

Credit Reporting Differences

How do these statuses appear on a credit report?

- Repayment: Reports as “Current” (or “Pays as Agreed”) as long as payments are made or the $0 IDR requirement is met.

- Forbearance: Reports as “Current,” often with a remark code indicating “Deferred” or “Payment Paused.” It is not a negative mark.

- Deferment: Reports as “Current,” typically with a specific “Student Loan – Deferred” remark.

While none of these statuses damage a credit score, lenders reviewing a report may treat them differently when calculating Debt-to-Income (DTI) ratios.

Some mortgage lenders may impute a hypothetical payment amount for loans in Deferment or Forbearance, assuming the pause is temporary.

Status Conflicts

Sometimes a dashboard may show conflicting information, such as a “Repayment” header but a “Forbearance” alert below it.

This usually happens during status transitions.

The servicing system updates in batches. If an account is moving from Repayment to Forbearance, the dashboard might display elements of both for 24–48 hours.

The “Loan Details” section typically contains the most accurate, real-time status code compared to the simplified summary screen.

This article provides general information about MOHELA servicing practices and federal student loan statuses. Individual account circumstances vary based on loan type, repayment plan, and relief classification. School Aid Specialists notes that specific questions about interest accrual or forgiveness eligibility for a specific status should be directed to MOHELA borrower services.

Sarah Johnson is an education policy researcher and student-aid specialist who writes clear, practical guides on financial assistance programs, grants, and career opportunities. She focuses on simplifying complex information for parents, students, and families.