Published: December 31, 2025

Works only if your debts were higher than what you owned right before forgiveness. If you were broke on paper, this is your escape hatch.

The calendar has turned, and the rules have changed. From 2021 through the end of 2025, many student-loan discharges were excluded from federal taxable income under the American Rescue Plan window.

Starting January 1, 2026, that federal exclusion generally ends unless Congress extends it.

If your student loans are forgiven under an Income-Driven Repayment (IDR) plan this year, the IRS may treat that canceled debt as taxable income. For a borrower with a $50,000 balance, this could mean an unexpected tax bill of $10,000 or more.

However, the U.S. tax code offers a specific protection. It is called the insolvency exclusion, and for many borrowers, it is the difference between financial ruin and a fresh start.

Worried about the tax bill? Use our free Student Loan Tax Bomb Calculator to estimate your insolvency.

The Reality of the 2026 “Tax Bomb”

To navigate this year’s tax season, you need to understand the trap most borrowers walk into.

For the last five years, a lot of borrowers never saw tax paperwork tied to forgiveness. That was the tax holiday. That holiday is over.

If a creditor cancels $600+ of your debt in 2026, they will generally file Form 1099-C with the IRS and send you a copy.

Do not ignore that envelope. If you toss it thinking it’s junk mail, the IRS can treat the canceled amount like taxable income. This is where Form 982 comes in. If you qualify for the insolvency exclusion, Form 982 is how you claim it.

(Note: If you met the forgiveness requirements in 2025, some borrowers may still get tax-free treatment even if the discharge posts in 2026 due to processing delays.)

Your bill depends on your tax bracket and state, so don’t lock onto a single number. This rule specifically targets borrowers on long-term IDR plans. It does not apply to Public Service Loan Forgiveness (PSLF), which is not considered income for federal tax purposes.

The Solution: What Is Insolvency?

The logic is simple: The government typically does not tax you on money you do not have.

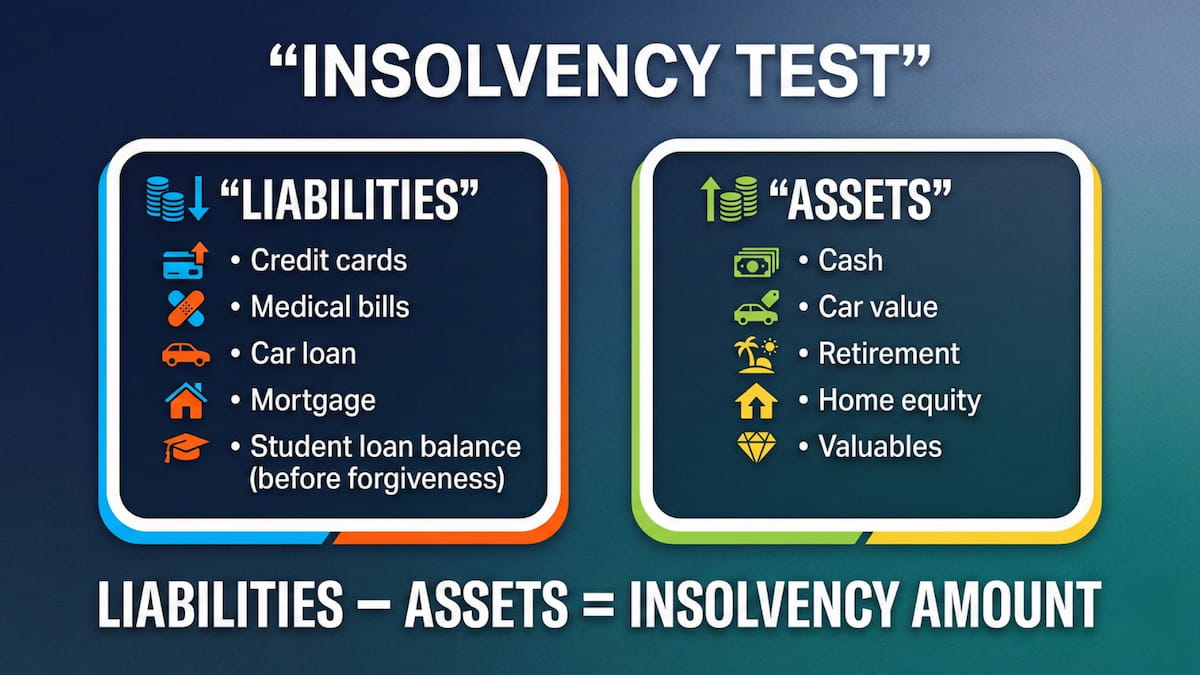

You are considered “insolvent” if, immediately before your debt is canceled, your total liabilities exceed the fair market value of your total assets. If you owe more than you own, you are insolvent. The IRS allows you to exclude canceled debt from your taxable income up to the amount of your insolvency.

How to Calculate Your Insolvency

Determining your eligibility requires a snapshot of your finances at the exact moment before forgiveness occurred. Use the Insolvency Worksheet in IRS Publication 4681 (you keep it for your records).

Step 1: Calculate Your Total Liabilities

List every single debt you owe. This includes:

- Credit card balances.

- Medical bills.

- Car loans and mortgages.

- Past-due utility bills.

- Crucially: The full balance of the student loan immediately before it was canceled.

Many borrowers make the mistake of leaving the student loan off this list. Including it is essential because it significantly increases your total liabilities, making it easier to prove insolvency.

Step 2: Calculate Your Total Assets

List the “fair market value” of everything you own. This is not what you paid for an item, but what you could sell it for today. This includes:

- Cash in savings and checking accounts.

- Real estate (home value).

- Vehicles.

- Retirement accounts (401k, IRA).

- Household goods and electronics.

The Magic Number: A Real-World Example

Once you have your totals, the math is straightforward. Subtract your Total Assets from your Total Liabilities. The result is your “insolvency amount.”

Imagine a borrower named Sarah. In June 2026, her remaining $50,000 student loan balance is forgiven.

- Liabilities: She owes $50,000 on the student loan, plus $15,000 in credit card debt and a $10,000 car loan. Total Liabilities: $75,000.

- Assets: She has $2,000 in savings, a car worth $12,000, and $5,000 in a 401(k). She rents her apartment. Total Assets: $19,000.

Sarah’s insolvency calculation: $75,000 (Liabilities) – $19,000 (Assets) = $56,000.

Since her insolvency amount ($56,000) is greater than the forgiven debt ($50,000), Sarah can exclude the entire $50,000 from her taxable income. She reports $0 taxable income from this cancellation.

(If you’re only insolvent by part of the forgiven amount, only that part is excluded — the rest is typically reported as income.)

How to File IRS Form 982

Qualifying is only half the battle; you must formally claim the exclusion. You cannot simply ignore the 1099-C. When you file your federal tax return, you must attach IRS Form 982 (Reduction of Tax Attributes Due to Discharge of Indebtedness).

On this form, you will typically focus on Part I, Line 1b, which checks for “Discharge of indebtedness to the extent insolvent.” You then report the amount of the canceled debt you are excluding from your income in Part I, Line 2.

Most filers also complete Part II to reduce tax attributes (such as basis in property), as required by the exclusion rules. By filing this form, you are telling the IRS: “Yes, I had debt canceled, but I was insolvent, so it is not taxable income.”

Take Control of Your 2026 Taxes

The return of taxable forgiveness is stressful, but it is not a dead end. For the vast majority of borrowers facing forgiveness after 20 or 25 years of payments, financial hardship is a reality. The insolvency exclusion is the legal mechanism designed to acknowledge that hardship.

If you receive a 1099-C this year, do not assume you owe the government thousands of dollars. Download the IRS Form 982 instructions, run the numbers, and verify if you qualify. In 2026, a little bit of paperwork is worth thousands of dollars in protection.

This article is for informational purposes only and is not tax advice. Rules vary by individual; always consult a CPA or tax professional before filing.

Sarah Johnson is an education policy researcher and student-aid specialist who writes clear, practical guides on financial assistance programs, grants, and career opportunities. She focuses on simplifying complex information for parents, students, and families.