⏱️ Read Time: 3 Mins

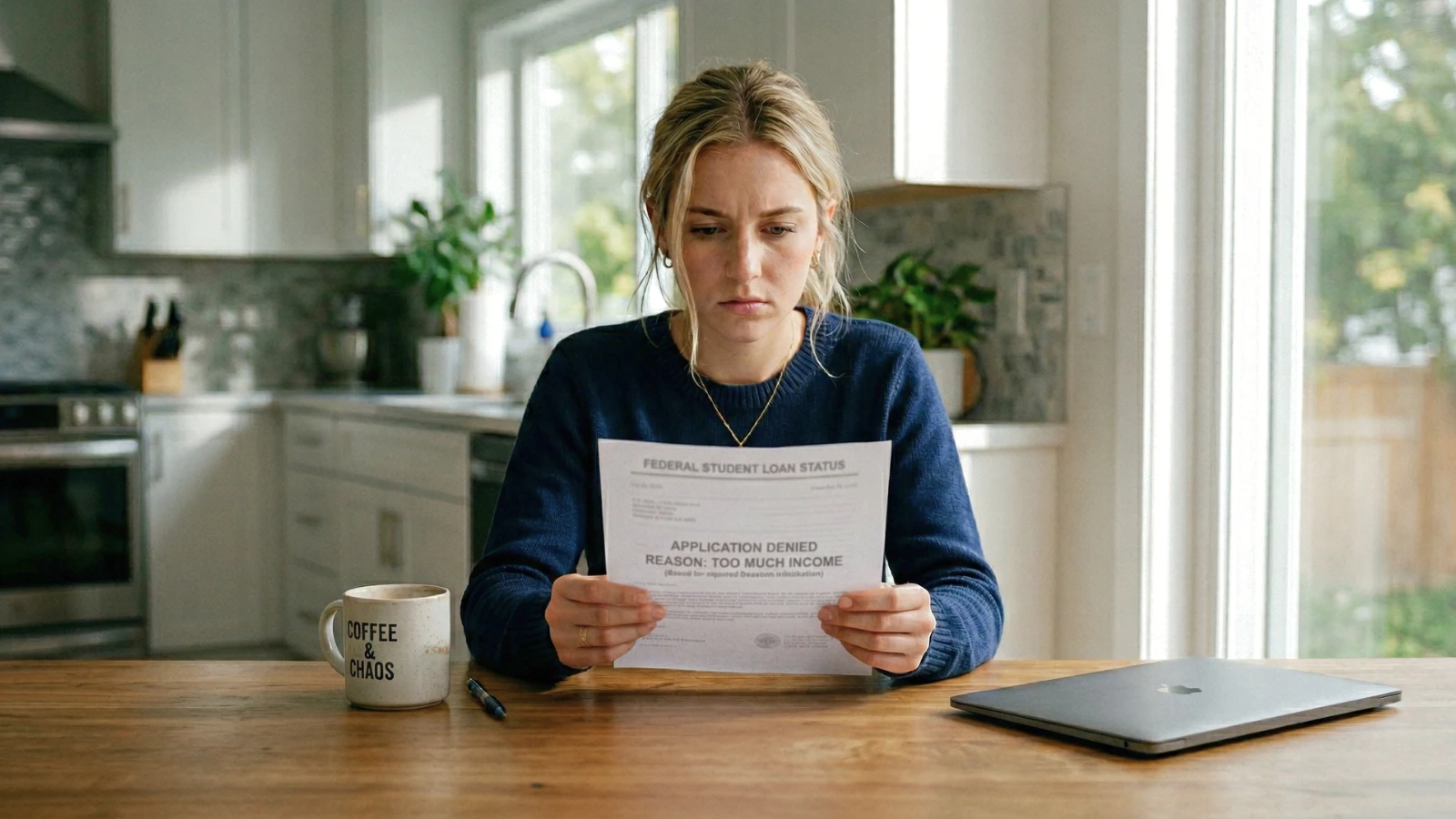

IBR rejections are becoming a common issue in 2026. Borrowers across the country are opening denial letters stamped with “no partial financial hardship” and wondering what went wrong.

Searches like “IBR denied too much income 2026” and “IBR application rejected what to do” show how widespread the issue has become.

Borrowers are being told they earn “too much” to qualify for relief, even when their budgets are already stretched. The result is confusion, higher payments, and no clear next step. Some borrowers are seeing approvals within days, while others get denied instantly for the same situation.

Why The System Is Rejecting You

Servicer systems have not been fully updated. Applications are still being processed with older rules. This mismatch is what causes the denial letters.

In many cases, your application is being evaluated using older eligibility checks instead of updated repayment guidance. That’s why you can be denied even when your situation hasn’t changed.

This also explains why different borrowers are getting different results at the same time. Some applications are processed correctly, while others are still caught in outdated filters.

What This Error Actually Means

In simple terms, your servicer may be using an outdated formula to judge your application.

Previously, IBR required a “partial financial hardship” — meaning your calculated monthly payment had to be lower than the standard 10‑year repayment amount. If you earned too much, you were denied.

Recent policy changes have shifted this requirement, but not all systems are updated consistently. Some borrowers are still seeing denials based on the old hardship test even though newer guidance allows broader access.

Getting this specific denial does not necessarily mean you are permanently disqualified. It often reflects a system lag or misapplied rule rather than your actual eligibility.

Why Some Borrowers Are Still Getting Approved

Not every application is being handled the same way right now. Some borrowers are getting approved because their application is processed under updated criteria, while others are still being evaluated using older rules.

This is why you might see people online saying they were approved in the same situation where you were denied. It is not necessarily about your income or eligibility, it is often about how and when your application was processed.

Immediate Strategic Moves

If you sit on this, the system will default you into a standard payment plan that’ll likely spike your monthly bill. Don’t let that happen.

Force a Reset Head back to the federal portal and submit a fresh IDR application. Doing this forces the current system to look at your file under the updated rules rather than the old ones.

Call and Demand Forbearance Get your servicer on the phone. Tell them point-blank your IBR denial was based on the “retired hardship” rule that no longer applies. Ask for a processing forbearance while they fix the mistake.

Escalate if Needed If the servicer starts giving you the runaround, go over their heads. File a formal complaint through the Federal Student Aid. Sometimes a formal paper trail is the only way to get a human to actually review a denial.

Track Everything Log every confirmation number and the exact date you hit “submit.” When the system glitches and it will, your documentation is the only leverage you have to prove they messed up.

Sarah Johnson is an education policy researcher and student-aid specialist who writes clear, practical guides on financial assistance programs, grants, and career opportunities. She focuses on simplifying complex information for parents, students, and families.