⏱️ Read Time: 3 Mins

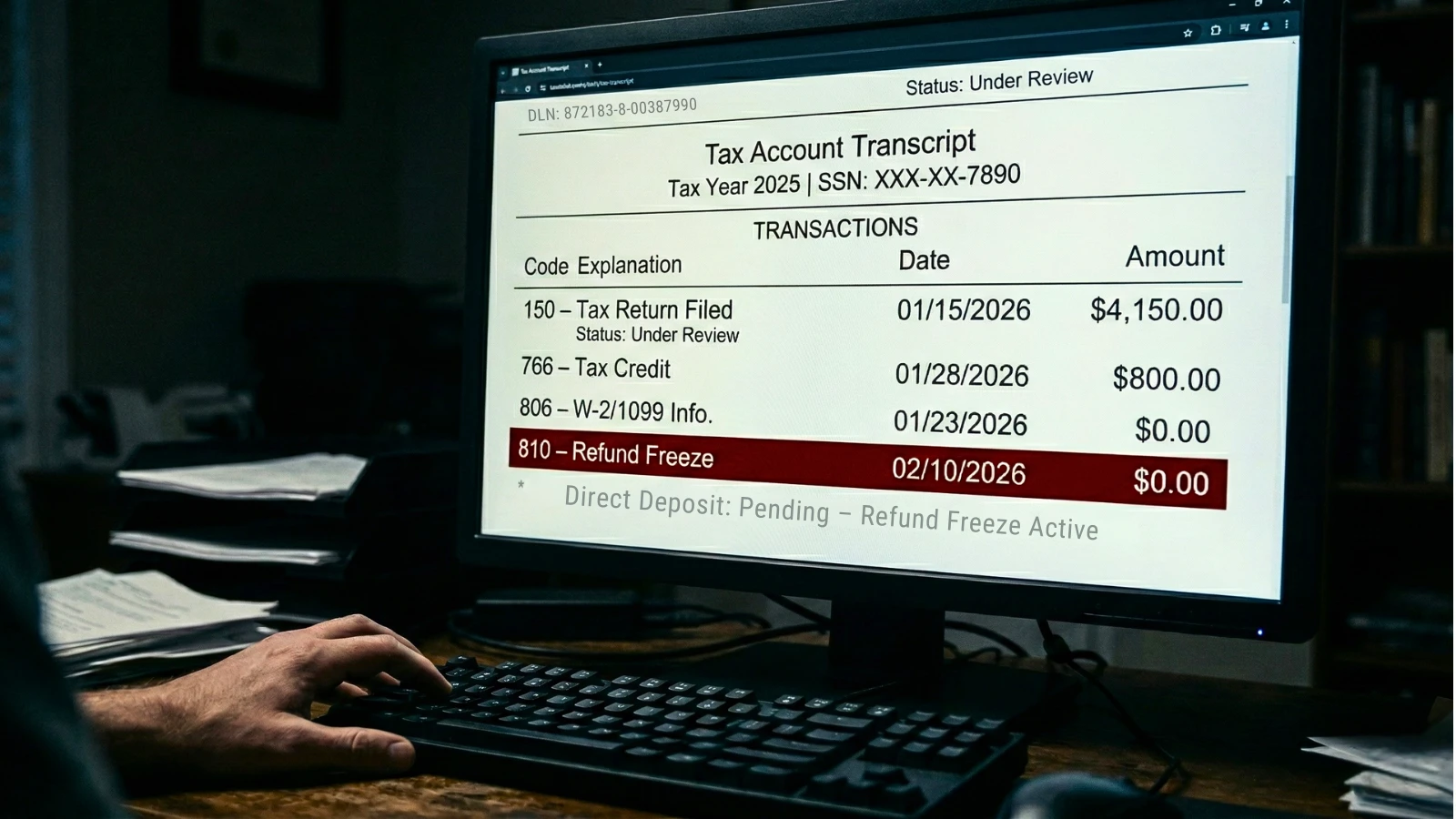

IRS transcripts showing Code 810 are currently stopping refunds before payment is issued. The freeze appears on taxpayer accounts without a direct deposit date and often surfaces weeks before any official notice arrives in the mail.

This is not a standard processing delay. It is a strict payout lock.

This systemic halt pulls a tax return off the standard automated processing line and routes it directly to a manual review queue.

The Mechanics of a Transcript Freeze

Code 810 functions as a hard stop inside the IRS processing system. When the automated system detects a significant discrepancy between the data claimed on a tax return and the institutional documents already on file, it suspends all payout activity.

This is fundamentally different from a routine identity verification delay. It signals that human examiners must review the numbers by hand before any money moves.

The hold persists until an agent resolves the mismatch and issues a subsequent Code 811 to officially release the funds.

Education Credits and the Cross-Reference Check

While sudden spikes in Schedule C business income or severe W-2 withholding mismatches can trigger an 810 freeze, education credits remain a primary catalyst during the spring filing season. The American Opportunity Tax Credit (AOTC) specifically draws heavy automated scrutiny for college students and their families.

The IRS verifies every AOTC claim directly against Form 1098-T.

Universities transmit this exact document to the government, reporting the total tuition billed in Box 1 and the total financial aid awarded in Box 5.

If a university reports that Pell Grants, state grants, and scholarships fully covered a student’s tuition bill, the student’s legally claimable out-of-pocket expense drops to zero.

When a tax return subsequently claims thousands of dollars in personal tuition expenses to secure the maximum $2,500 AOTC, the internal system catches the math failure. The automated cross-check flags the mismatch, blocks the credit, and immediately freezes the entire tax refund.

The Processing Blind Spot

The most difficult phase of an 810 freeze is the immediate silence. Taxpayers often spot the code on their digital transcripts well before the IRS drafts and mails a physical explanation.

During this gap, the public-facing “Where’s My Refund?” tool offers limited transparency. It typically strips away the target direct deposit date and replaces it with a generic processing delay message, often pointing to Tax Topic 152.

Attempting to resolve the hold by calling the main IRS support line during this period is largely ineffective. Telephone representatives cannot bypass an active transcript freeze. They are instructed to verify that the return is in the review department and advise the taxpayer to watch the mail for correspondence.

The CP05 Notice and the Wait

The review process eventually results in a formal notice. For an 810 hold, this is frequently a CP05 notice.

This letter officially notifies the taxpayer that the agency is verifying their income, withholding, or claimed tax credits. The standard CP05 notice does not immediately demand receipts.

Instead, it instructs the taxpayer to do nothing and wait up to 60 days while examiners attempt to verify the return internally.

If the internal review fails to clear the discrepancy, the IRS escalates the process. They will issue a follow-up request, often a CP05A, demanding physical proof to back up the tax return.

The Documentation Demand

Navigating this secondary phase requires exact documentation. A simple bank statement showing a generic withdrawal is rarely enough to clear an education credit audit.

Examiners demand highly specific proof that the taxpayer paid out-of-pocket for qualified expenses. This means producing official university ledger prints, direct billing statements, and itemized receipts for required textbooks and specialized software.

If a taxpayer cannot physically prove their expenses exceeded the financial aid reported on their 1098-T, the IRS will deny the AOTC claim.

Filing an amended return out of panic while an 810 freeze is active generally complicates the process, forcing the system to reconcile two different returns while still under a manual review block.

The agency will eventually remove the freeze, but only after recalculating the final tax liability. This adjustment typically results in a heavily reduced refund minus the disallowed credits, or a final bill for taxes owed. Securing university billing statements and physical receipts the moment an 810 code appears remains the most effective way to prepare in case a documentation request follows.

Sarah Johnson is an education policy researcher and student-aid specialist who writes clear, practical guides on financial assistance programs, grants, and career opportunities. She focuses on simplifying complex information for parents, students, and families.